"Transitory inflation"

What’s a couple trillion dollars in printed money between friends?

From Fox Business:

Producer prices accelerated at the fastest annual pace on record in July as supply chain disruptions and materials shortages continued to put upward pressure on costs.

The producer price index for final demand increased at a 7.8% pace for the 12 months ended July, according to the Labor Department. The July print was faster than the 7.3% pace recorded in June and ahead of the 7.3% rate that analysts surveyed by Refinitiv were expecting. The reading was the strongest since recordkeeping began in November 2010.

Article link: https://www.foxbusiness.com/markets/producer-price-index-july-2021

I realize I have a mix of an audience and some followed me from my old CFA Program content, some followed because of my crypto content, and some followed because of my military content. I’ll put the above blurb in plain English: this isn’t normal. At all.

The standard definition of inflation is the consumer price index, not the producer price index, but PPI is worth noting because these costs will likely start trickling down to consumers in CPI. The industry standard “long term” planning factor for inflation I’ve always seen as 2.5%.

And PPI change was 7.8%.

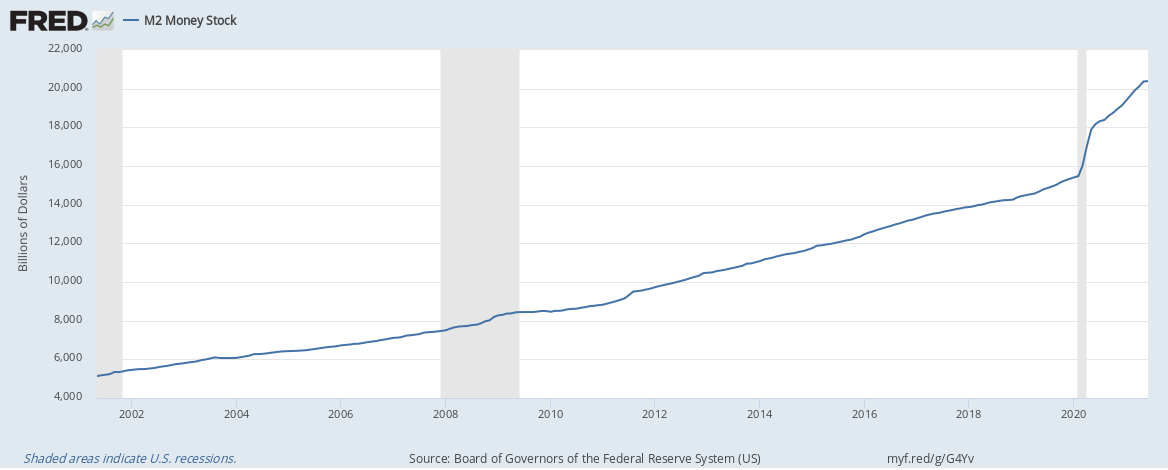

Honestly though, this shouldn’t be a surprise. We’ve been going through an unprecedented monetary experiment since the 2008 crisis and quantitative easing, and we only stepped on the gas even harder in March 2020 with COVID. Below is the M2 Money Supply of US Dollars, from Federal Reserve Economic Data:

What’s a couple trillion dollars in printed money between friends? To be clear, I’m not bashing on just the US Fed since pretty much every central bank has been doing the same (ECB, JCB, etc.), and perhaps after 2008 such measures were needed to prevent another Great Depression.

At what point though does this start having second and third order effects?

Considering how crypto was nonexistent in 2009 and now is a $1.87 trillion asset class according to CoinMarketCap as of today’s data (August 12, 2021), and considering these PPI numbers, I’d say right about now.

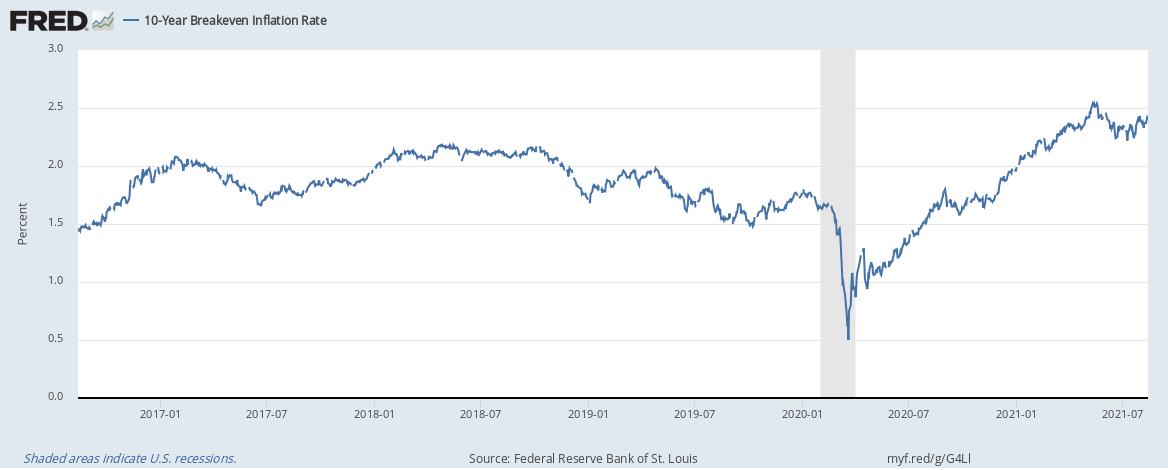

There is one thing that leaves me curious. Bond traders and economists would use the spread between 10 year Treasuries and 10 year TIPS (Treasury Inflation Protected Securities, meaning, special Treasury bonds that adjust their payment based on inflation) as a way to predict inflation. The idea was that economists may or may not be right on their forecasts, but this is a way to see the wisdom of the market and how asset allocators are making real decisions with capital deployment to discern inflation expectations.

As of today (August 12, 2021), that market derived inflation expectation rate is 2.41%, according to Federal Reserve Economic Data.

To me, this says more about the current state of the bond market and how Fed purchases have had a disruption, rather than long term inflation expectations. 2.41% is a “normal” number. This just does not make sense contextually with a 7.8% PPI.

If only we had some other kind of asset class, some kind of digital alternative to both precious metals and traditional fiat currencies…

-Alex